When you’re in a pinch, short-term loans seem like a good idea. Although they promise a short-term cash fix, they too often become a ‘debt hangover’ leaving you wondering where you went wrong. While short-term cash loans, often referred to as payday loans, can be a helpful tool when used correctly, you need to be aware of the details and responsibilities involved, as well as the alternatives available.

Payday loans are some of the most expensive personal finance options you’ll come across, so it pays more than anything to do your research and shop around for the best solution. In this article, we’ll take a look at the fundamentals of payday lending, the risks involved as well as a meaningful alternative, pay on demand, that takes a different approach to bridge short-term cash issues in a more sustainable manner.

How payday loans work

A payday loan is a type of credit whereby the borrower must repay the loan within 12 months and often much shorter. Some payday loans must be repaid in as little as sixteen days, in line with the pay they receive from their employment (hence the name). In turn, payday loans are only offered to borrowers with a job that they can verify.

Each provider (such as Credit24) varies with the terms that they offer; however, there are strict limits on what fees can be applied and what interest is chargeable. For instance, borrowers can apply for loan amounts of no more than $5,000. The borrower is usually charged a base 20% ‘loan establishment’ fee, in addition to a monthly interest charge. The limits are put in place by ASIC, which has a role to play in regulating the fair financial play of lenders in Australia.

The maximum interest charge (or ‘service fee’) is 48% per annum, or 4% a month (based on the principal amount borrowed). Given this fee is capped, most providers will simply charge the maximum amount. Some will offer cheaper alternatives, but they come with their own requirements that you will need to check on an individual basis. It’s also important to remember that although payday loans are unsecured, often the lenders (esp. Offline payday loan providers) may ask to hold a ‘deposit’ in the form of a valuable asset owned by the borrower. In practice, this means that non-payment will result in a serious mark on your credit report, as well as putting at risk any assets that you have provided them.

Payday loans are an expensive type of loan, and they’re best used for fast money needed to settle bills you weren’t planning for. If used long-term, there are many risks that may arise, primarily from the high fees and structure of the industry.

Extremely high fees. It’s no secret that the charges associated with a payday loan are through the roof. In the past, payday lenders were opportunistic and preyed on those in need. Now, there are limits on fees and charges, although they are still much higher than traditional loans or other forms of credit, even credit cards. There are various fees involved, including charges for late payments or even defaulting on the loan. Some payday lenders still charge more than they’re legally allowed, so do your research.

Short timeframes with large payments. Since the repayments are tied to your “payday”, the lender may be entitled to a large portion of your paycheck. This will depend on the length of the loan and how much each of your repayments are. Missed payment (and the associated late fees) could be highly detrimental to your already fragile financial position.

Dangerous and illegitimate lenders. The payday loan industry has a dark history. It is thought that the origins of payday lending stem from the practices of the ‘loan shark,’ whereby lenders would use force and threats to extort victims of their money. While legally operating payday lenders are not like this today, they are sometimes still lumped into the same category. If you are going to use a payday loan, make sure the lender is legitimate and operates under the law, as for any financial service.

Debt traps and worsening credit. If you don’t pay the loan back on time, it can be difficult to then meet the repayment, plus extra late fees. Too often, this leads to customers falling into a cycle of debt that is hard to escape from, with the interest and fees quickly ballooning to multiple times the original borrowed amount. Worse still, missed payments show up on your credit report, making it harder for you to get credit on good terms in the future.

If you cannot make a repayment on time, you will be liable for default fees and enforcement expenses (to cover the cost of recovery). Under the current law, the maximum you can be charged is double the amount you borrowed – which is still a hefty amount!

Are payday loans a bad idea?

Whether or not payday loans are good or not depends on your situation, but it is almost certainly bad compared to other alternatives in the market. As a short-term or once-off financial fix, then they can certainly help in a bind. If you find yourself returning repeatedly, it’s a better idea to consider a more sustainable alternative.

Longer-term options include effective budgeting, secured credit from a bank, savings, and borrowing from family and friends. During this process, there are other, better alternatives to payday loans that may work better for you – one of these options is ‘Earned Wage Access’.

How a healthier and more ethical alternative like Earned Wage Access works

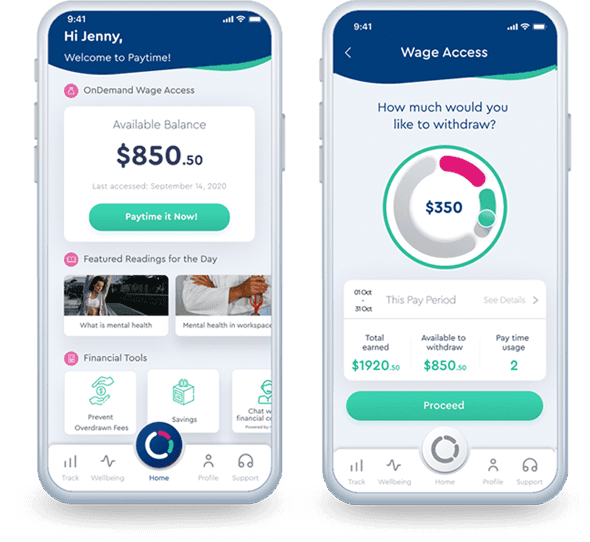

Earned Wage Access usually comes in the form of a simple-to-use app that give employees quick access to a part of their next paycheck. These apps will connect to your employer’s payroll and time-and-attendance systems in order to calculate how much wages you have earned, and therefore be able to withdraw.

Users can only access a portion of the amount that they have already worked for (and therefore earned) but not yet paid. This amount will later be deducted from your payslip on payday, and you will receive the remaining amount. As such, it is not a loan – and there will be no credit checks done nor any impact on your borrowing capacity from utilising Earned Wage Access.

Since this service is put into place by your employer, you first need to check if your employer offers this kind of service within the organisation. If it does not offer Earned Wage Access, we encourage you to reach out to HR and tell them that you would like this solution to be offered to you and the rest of your colleagues. An example of such a provider is Paytime, so by providing HR (or your CFO) with the details then they can be fully informed. At the same time you as an employee of the company should also contact the Earned Wage Access provider (like Paytime) directly, for them to also reach out to HR to arrange a free consultation on the solution in order to get it implemented in your company.

In addition, as it is an employer offered solution and is not a loan, Earned Wage Access is far cheaper and more efficient than any other types of finance. At times, this solution can be offered for free to the employee when subsidised by the employer, as an employee benefit.

What’s the difference between payday loans and Earned Wage Access?

There are huge differences between the two. Payday loans are short term loans that charge interest and high fees and can get people stuck into debt, whereas Earned Wage Access is the ethical alternative. Earned Wage Access is not a loan, as it simply allows you to access a portion of your wages that you have already earned, but not yet paid.

Earned Wage Access is the better option as it promotes a more sustainable approach to achieve financial wellness and stay out of debt. Earned Wage Access is not a loan, there’s no interest charged and there is nothing to repay.

Get The Heathier Alternative!

No one should wait 15-30 days to receive

their hard earned pay, it’s time for Earned Wage Access.