Not a loan to the employees.

Earned Wage Access is not considered a loan to the employees as they can only access what they have earned and worked for – what is rightfully theirs. Employees who have not worked will not be able to withdraw anything on the Earned Wage Access app as the balance will reflect as Nil.

A safety net for your employees.

Earned Wage Access is not a solution designed to be used daily. Rather, it is more of a ‘safety net’ that companies can provide to their employees for free that helps them if they’re ever in a cash flow pinch. This way, you can help your employees stay out of predatory lending/payday loans when they are short of cash, and therefore, saving them thousands of dollars of debt and headache.

Prepares you to be a Workplace of the Future.

As the world moves to a more instantaneous, digital one, allowing employees to access the money that they have earned without forcing them to wait until payday will be something that will be demanded by the workforce. Do not be a follower on this field, or else your employees may consider leaving to competitors that offer it first.

Configurable guardrails and limits.

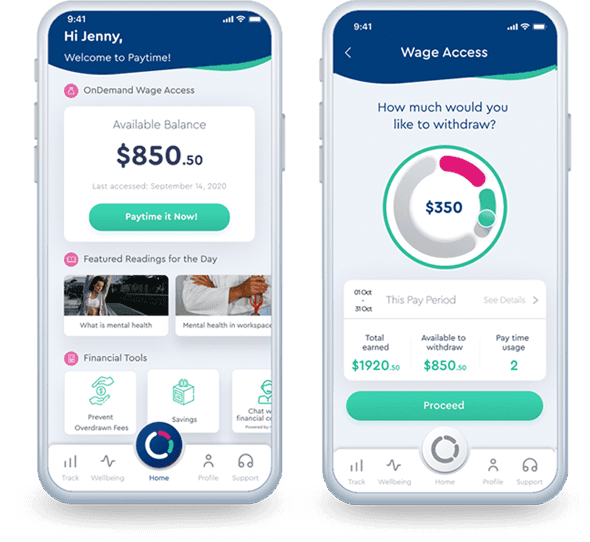

The employer has full control on what is considered ‘safe usage’ and therefore can place guardrails and limits as they see fit. For example, the available balance can be set at 50% of employees’ earned wages to ensure that they still have some amount remaining to be paid out on payday. Employers also can put a limit on the number of withdrawals per month, or a maximum dollar limit per withdrawal, if they feel it necessary.

No manual work, or change to the way companies do payroll.

Earned Wage Access providers integrate their apps and system so seamlessly with companies’ payroll and time-and-attendance software such that there is no need for any manual interventions. All the deductions are posted automatically to payroll, and employees will be paid their outstanding amount automatically on payday.

No repayment or recourse back to the employee.

Since no money is being lent, and since repayment is taken care of within payroll (through deductions) – there is no repayment or recourse back to the employee. However some Earned Wage Access providers still do impose a recourse on the employee, such that they have the right to debit the employee’s account. Reading the fine print carefully will help you understand what the implications are for your employees, so be careful to choose a provider that does not require any repayment of the funds from the employee nor recourse back to the employee, in the event that the employer does not repay the Earned Wage Access provider on payday.